“Sensitivity Analysis is a very useful technique to identify main variables that is influencing decisions and impact on value of the projects with probable change in such variables. Impact of change will be sensitive when investment decisions are influenced by the results of change in variables.”

Tools like Discounted Cash Flow, Payback Period, Net Present Value, Internal Rate of Return (IRR), etc. are widely used in investment decisions. All these tools are calculated on the basis of net cash flows over the life of the project.

Most of these financial tools used for analyzing investment decisions are based on cash flows of the project basically net operating cash flows (cash inflows less cash outflows). It means cash flows related with finance are ignored because they are represented by cost of capital which is used to discount those operating cash flows. Various variables are used to derive net cash flows from the project. They are basically sales units, selling price, raw material cost, labour cost, other operating costs (normally overheads), taxes on operating profit, etc.

Remember, net cash flows from the project does not depict operating profit from the project because operating profit statement also includes non-cash items like depreciation. But profit statements are used to arrive at net cash flow from operations after adjusting non-cash items from net profits.

In addition to operating cash flows, other project related relevant costs are included in cash flows of the project such as cost of the project, working capital investment required, disposal value of project, etc. After deriving net cash flows by including all the cash inflows and cash outflows together, these are then discounted by project’s cost of capital in order to derive net present value of the project. Net Present Value (NPV) is mentioned here because NPV is the superior financial tool to analyze investment decisions although other tools like Payback Period and IRR also used in many analyses.

Cash flows derived for the purpose of arriving at investment decisions are all forecasted cash flows. Most likely assumptions are made about all the variables used in deriving net cash flows in future. Those assumptions are based on current facts and figures and future expectations of business and economic environment. It is not sure that these assumptions will hold true over the life of the project. Thus, there are uncertainties about the outcome of the project in terms of cost, volume, pricing and cost of capital.

However, those variables can be quantified in some ways on the basis of past experiences or probabilities of their occurrences. Scenarios can be drawn for best possible, most likely and worst case conditions. Basic calculations and analysis are done for most likely condition. Best possible condition is not troublesome because they will enhance value of investors. But worst case conditions are worth evaluating for reconsideration. Risk persist in worst case conditions. Thus, evaluation of investment decisions under worst case scenario is called Investment Appraisal under risk. This analysis is based on “what if analysis” and precisely known as Sensitivity Analysis.

Sensitivity Analysis is a very useful technique to identify main variables that is influencing decisions and impact on value of the projects with probable change in such variables. Impact of change will be sensitive when investment decisions are influenced by the results of change in variables. As we are discussing about most suitable investment analytical tool i.e. NPV, we should be aware about decision criteria of NPV. This is simple because if NPV of the project is positive the project is worth undertaking and if it is negative it shall not be healthy decision to undertake such projects because negative NPV will eat shareholders’ value. Hence, NPV being zero is hurdle point for investment decision.

Zero NPV shall not eat shareholders’ value but shall not contribute to it as well. So, any change in variable that brings the most likely NPV down to zero will be the concern for any investor. In sensitivity analysis, we shall identify the least changes (in a percentage term) of a particular variable that bring the NPV to zero.

The outcome of sensitivity analysis will draw management attention about most important variables to consider before concluding investment decision. Thus, when we are not sure about the forecasted cash flows in future or NPV derived is so small in comparison to investment amount that changes in any variable can have significant impact on NPV and also can impact the decision taken by investors.

Let us make this clear with following example:

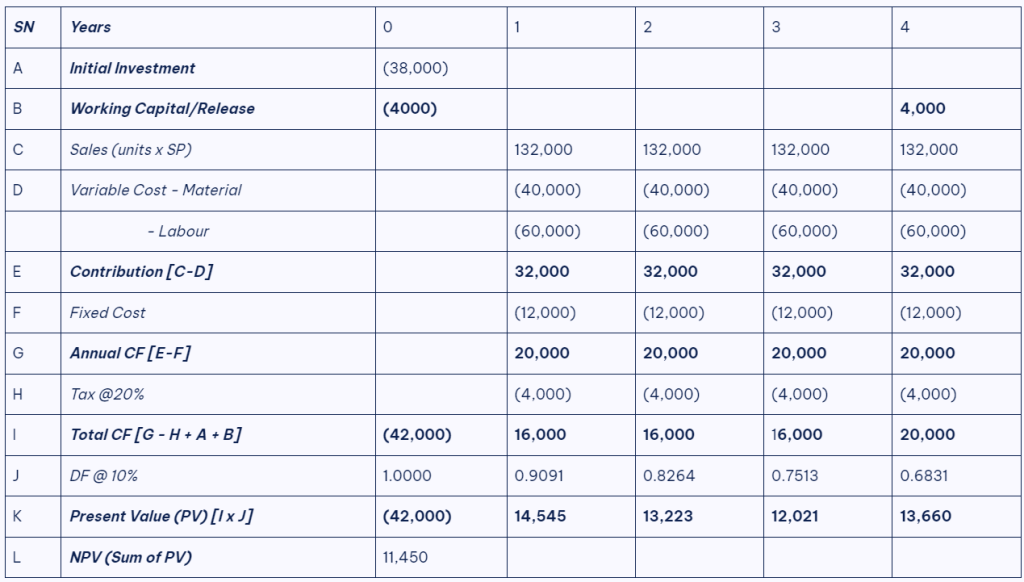

Example: A companyassumes an investment of $38,000 in an OTC license today and is expected to give annual contribution of $32,000 for next 4 years. This is based on selling one product, with a sales volume of 10,000 units, selling price of $13.20 and variable costs per unit of $10. Annual fixed cost of $12,000 (assume all cash) will be incurred for the next four years; the discount rate is 10%. The investment requires working capital of $4,000 at beginning of the project which shall be released at the end of the project. The corporate tax rate is 20%. Ignore amortization of investment and its tax saving.

Let us calculate the NPV of this investment on the basis of most likely forecast given above.

The NPV Calculation on the basis of information given above:

NPV of the project is $11,450. The project is viable as it adds to the value of the firm. However, the acceptability of project is based on forecast of various variables that must hold true and correct for next four years. The analyst has provided further information about various variables as below:

- Initial Investment: License is being issued by Government and review of license cost is being discussed at cabinet. If Government decides to increase the cost of license, this may go up by 20%.

- Selling price of product: There are few competitors in the industry who have spent several years in this industry. They are operating at full economies of scale. If this project is undertaken, they can decrease their selling prices as they can maintain total contribution equal to us at low price because of their volume. The Managing Director wants to know at what level we are prepared to cut down prices if price wars persist.

- Variable cost of product: Variable cost includes 40% of material cost and 60% labour costs. There are limited suppliers of raw materials and chances are that they can increase material prices by 10%. Similarly, wage rate was just increased last year but labour union are demanding at least 5% increase in wage rate to cope with high inflation in basic goods.

- Sales volume: There is increased competition and also increasing taste of the customers so there is probability that sales demand can fluctuate by 15% both sides.

- Annual fixed cost: Fixed cost includes salary of supervisor and engineers and they have high demand in the market. But they can be available and retained if they are paid 15% higher than current expectation.

- Discount rate used: The project will be partially financed by debt which is based on LIBOR plus premium. In next four years the LIBOR is expected to fluctuate ups and downs causing cost of capital to fluctuate by not more than 15% from current cost of capital.

- Working Capital Investment: Due to severe competition credit period may be allowed higher than current expectations to customers in order to boost sales and this can double the working capital requirement.

- Tax rate: The Finance Minister, in an interview has stated that corporate tax in this country is very low in comparison to nearby other similar countries. The corporate tax is 30% in most of the nearby countries.

There are uncertainties in each of the variable weather it be cash inflows or cash outflows. Uncertainty creates risk to the NPV. Variables causing decrease in revenues and increase in costs is risk to the viability of the project. Here, we have to analyze the project viability in terms of risk inherent in each of the variables i.e. increase in cost (cash outflow) or decrease in revenue.

When evaluating the project in terms of project variable, we consider only one variable to happen and other variable remain constant although there is a probability of changing more than one variable at a time. Changes in more than one variable must be analyzed by other method of investment analysis tools like scenario analysis or simulation.

Now the question is how we perform sensitivity analysis in the given example. We are concerned about deviation in variables from our expectation which brings our NPV down. As project shall not be selected when NPV will be less than zero (i.e. negative); concern for analyst will be Zero NPV that is resulted by changes in any particular variable. So, we shall compute the maximum tolerable limit in terms of percentage of particular variable changes. For that computation, we need to analyze the negative contribution in present value terms caused by changes in such variable. Negative contribution in NPV is supported by decrease in selling price or volume and increase in production costs, operating costs, taxes or discount factor.

The investor will be sensitive when negative contribution causes current NPV to come down at zero. It is because if NPV is below zero (negative), the decision of the investor will change. So, changes in variable will negatively contribute to existing NPV and such negative contribution is tolerable to the extent of current NPV. Thus, sensitivity of any variable is calculated as:

Sensitivity analysis formula

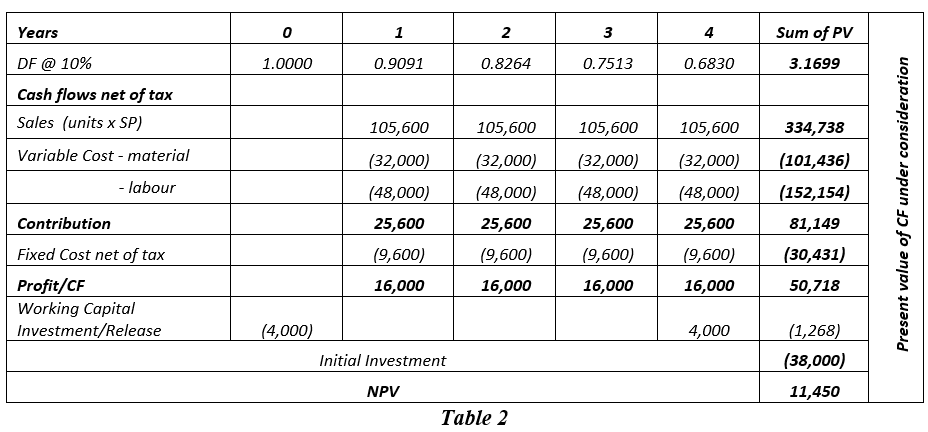

As present value of cash flow of each variable under considerations are important to contribute NPV of the project positively or negatively, it will be easier to compute NPV of the project in following ways to understand how net of tax cash flows of each variable is impacting NPV of the project:

Let us discuss the sensitivity of each of the variable that is affecting OTC’s NPV in the above example:

- Initial Investment:

License cost is $38,000 now which is expected to increase by 20%. If license cost does not change, the project’s NPV will be $11,450. If it increases NPV will come down. As all the investments are expected to be incurred at time zero, current negative contribution of investment in present value terms is $38,000. If this negative contribution in present value terms increases by $11,450, the NPV will be zero. It means increase in investment by $11,450 from current investment of $38,000 will be 30.13% ($11,450/$38,000).

The conclusion is investment has sensitivity level of 30.13% i.e. the decision about project selection will be affected when project’s investment exceeds 30.13% from current level. As there is a chance that cabinet will increase license cost (project cost) by 20%, however that does not affect the OTC’s investment decision because the NPV of the project will be reduced but shall remain above zero level as 20% shock level is less than 30.13% tolerable level.

- Selling price of product:

We have to calculate by how much the selling price is contributing to OTC’s NPV. Sales figure of the project is dependent upon selling price of the product. The present value of sales is the contribution amount attributable to NPV. Sales figure per annum for the next 4 years is $132,000. Sales will contribute to profit hence it will attract corporate tax. So, after tax sales figure for the next 4 years will be $105,600 per annum (see table 2).

The present value of after tax sales value will be $105,600 x PVIFA@10% for 4 years = $105,600 x3.1699 = $334,738. The sales is contributing positively by $334,738 to NPV. If the selling price falls, the present value of net sales will fall and ultimately NPV will be reduced. However, present value of net sales must not fall by more than the NPV amount i.e. $11,450. So, sensitivity of selling price will be equal to $11,450/$334,738 i.e. 3.42%.

The conclusion is selling price is more sensitive because only 3.42% reduction in selling price [$13.20 x (1-3.42%) = $12.45] will bring the current NPV to zero. As competitors are at competitive position due to their economies of scale, they are likely to decrease their selling price but OTC’s project will not be financially viable as it cannot reduce its selling price in larger proportion (not more than 3.42%). Thus, company must further analyze possibility of current expected selling price to change by the competitor before undertaking the project.

- Variable cost of product:

Variable cost has two component viz. material and labour.

Sensitivity of material:

We have to calculate by how much the material price is negatively contributing to OTC’s NPV. Variable cost of the project is dependent upon material price of the product. Material cost per annum for the next 4 years is $40,000. Material cost will negatively contribute to profit hence it will save corporate tax. So, after tax material cost for the next 4 years will be $32,000 per annum (see table 2).

The present value of after tax material cost will be $32,000 x PVIFA@10% for 4 years = $32,000 x 3.1699 = $101,436. The material cost is contributing negatively by $101,436 to NPV. If the material cost rise, the present value of material costs will rise and ultimately NPV will be reduced. However, present value of material cost must not rise by more than the NPV amount i.e. $11,450. So, sensitivity of material cost will be equal to $11,450/$101,436 i.e. 11.29%.

The conclusion is 11.29% increase in material price [$4 x (1+11.29%) = $4.45] will bring the current NPV to zero. There is possibility that material cost will rise by 10% but investment decision will be sensitive or thinkable when the material cost rise by 11.29%. The NPV of the project will still be positive although material cost rise by 10%. However, the sensitivity level is not so far from possible rise of material costs (10% vs 11.29%). Investment decision must be thoroughly analyzed in terms of material cost forecasting because material cost which is expected to rise by 10% can possibly rise by 11% or so resulting NPV at marginal level for changing our decision criteria.

Sensitivity of labour:

Sensitivity of labour can be computed similar to material. The present value of after tax labour cost will be $48,000 x PVIFA@10% for 4 years = $48,000 x 3.1699 = $152,154. So, sensitivity of labour cost will be equal to $11,450/$152,154 i.e. 7.53%.

The conclusion is 7.53% increase in labour cost [$6 x (1+7.53%) = $6.45] will bring the current NPV to zero. As wage rate was increased last year and labour union’s demand is 5% minimum; it is unlikely that labour cost will increase more than 5%. So, the project will be financially viable although labour cost rises by 5% because the tolerable limit of rise in labour cost is 7.53% (i.e. sensitivity) for this project.

- Sales volume/quantity:

We have to calculate by how much the sales volume is contributing to OTC’s NPV. Sales figure of the project is dependent upon sales volume of the product. The present value of sales will positively contribute to NPV. But, sales volume/quantity will also drive variable cost of the product which contribute negatively to NPV. Thus, sales volume will have impact over contribution margin (i.e. sales less variable cost). Sales volume/quantity will result contribution margin of $32,000 per annum for the next 4 years. Contribution will attract corporate tax. So, after tax contribution margin for the next 4 years will be $25,600 per annum.

The present value of after tax contribution margin will be $25,600 x PVIFA@10% for 4 years = $25,600 x3.1699 = $81,149. If the sales volume falls, the present value of net contribution margin will fall and ultimately NPV will be reduced. However, present value of net contribution margin must not fall by more than the NPV amount i.e. $11,450. So, sensitivity of sales volume will be equal to $11,450/$25,600 i.e. 14.11%.

The conclusion is 14.11% reduction in sales volume [10,000 x (1-14.11%) = 8,589] will bring the current NPV to zero. Due to increased competition there is possibility that sales demand can fluctuate by 15% both sides. Upside demand is not risk to the project but downside demand will have problem to project’s viability. If demand falls by 15% from current level of expected sales volume as stated, the project’s NPV will be negative and will not be viable because tolerable limit of sales volume (sensitivity) is 14.11%. Thus, this project shall not be undertaken unless there is possibility that the sales demand shall not be less than 8,589 units (i.e. less than sensitive level of 14.11%).

- Annual fixed cost:

Fixed cost will be negatively contributing to OTC’s NPV. Fixed cost per annum for the next 4 years is $12,000. Fixed cost will negatively contribute to profit hence it will save corporate tax. So, after tax Fixed Cost for the next 4 years will be $9,600 per annum (see table 2).

The present value of after tax Fixed cost will be $9,600 x PVIFA@10% for 4 years = $9,600 x 3.1699 = $30,431. The Fixed cost is contributing negatively by $30,431 to NPV. If the Fixed Cost rise, the present value of fixed costs will rise and ultimately NPV will be reduced. However, present value of fixed cost must not rise by more than the NPV amount i.e. $11,450. So, sensitivity of fixed cost will be equal to $11,450/$30,431 i.e. 37.63%.

The conclusion is 37.63% increase in fixed cost [$12,000 x (1+37.63%) = $16,515] will bring the current NPV to zero. There is possibility that fixed cost will rise by 15% but investment’s sensitivity in terms of fixed cost is 37.63% far from expected increase i.e.15%. Thus, Investment decision shall not be affected by possible changes in fixed cost and so is less sensitive.

- Discount rate used:

In other variables, we calculated impact on current NPV due to changes in any variable on cash flow of the project. Impact on cash flow were calculated at present value terms discounting such cash f lows at cost of capital. Now we are discussing about changes in such discount rate which will have impact over all the cash flows (net of inflows and outflows). But our concern is at what rate of discount factor, the present value of cash flows will be zero. This is the rate basically we are familiar with i.e. internal rate of return (IRR). So, we need to calculate IRR of the project.

Thus, IRR of the project’s cash flow is 21.63% which can also be calculated by interpolation method. It means project is expected to give return of 21.63% and if cost of project (financing cost) increases to 21.63%, then nothing remains in value i.e. NPV will be zero at 21.63% cost of capital. Thus, sensitivity is computed for percentage increase in cost of capital from current 10% to 21.63% i.e. [(21.63%-10%)/10% = 116.30%].

The conclusion is project cost of capital (discount factor) must rise by 116.30% from current level to come down NPV at zero. Due to rise in LIBOR rates, cost of capital may increase but not more than 15% rise is expected. So, sensitivity of 116.30% (tolerable limit) is much higher than 15% (worst case expectation). The project is less sensitive in terms of rise in discount rate.

- Working Capital Investment:

Working capital investment will negatively contribute to OTC’s NPV at the beginning and positively contribute to NPV at the end.

The present value of Working capital investment will be ($4,000) + $4,000 x PVIF@10% for 4 years = ($4,000) + $4,000 x 0.6830 = ($1,268). The Working Capital Investment is contributing negatively by $1,268 to NPV. If the Working Capital Investment is increased, its present value will rise and ultimately NPV will be reduced. However, present value of Working Capital Investment must not rise by more than the NPV amount i.e. $11,450. So, sensitivity of Working Capital Investment will be equal to $11,450/$1,268 i.e. 903.03%.

The conclusion is 903.03% increase in Working Capital Investment [$4,000 x (1+903.03%) = $40,121] will bring the current NPV to zero. There is possibility that Working Capital Investment will rise by 100% (double) but investment’s sensitivity in terms of Working Capital Investment is 903.03% far from expected increase i.e.100%. Thus, Investment decision shall not be affected by possible changes in Working Capital Investment and so is less sensitive.

- Tax rate:

Tax rate will negatively contribute to OTC’s NPV. The taxes paid at current tax rate is $4,000 for each of the next four years. The present value of taxes paid will be $4,000 x PVIFA@10% for 4 years = $4,000 x 3.1699 = $12,679. The tax payment is contributing negatively by $12,679 to NPV. If the tax rate is increased, the present value of tax amount will rise and ultimately NPV will be reduced. However, present value of tax amount must not rise by more than the NPV amount i.e. $11,450. So, sensitivity of Tax rate will be equal to $11,450/$12,679 i.e. 90.30%.

The conclusion is 90.3% increase in Tax rate [20% x (1+90.30%) = 38.06%1] will bring the current NPV to zero. Considering the tax rate applicable at nearby countries, there is possibility that tax rate will rise up to 30% but tolerable limit is 38.06%. Thus, Investment decision shall not be affected by possible changes in tax rate and so is less sensitive.

In summary, sensitivity analysis plays vital role in investment decision making. It gives the analyst the maximum tolerable limit in percentage terms that can be accommodated with the changes in certain variable. Sensitivity analysis will be helpful in decision making and investment analysis in the following ways:

Identification of key variables: It helps to identify key variables that is more sensitive to influence decision in investment appraisal. Suppose, selling price in the above example is more sensitive because only 3.42% changes (reduction) in selling prices can bring the NPV to zero resulting the project not viable for investment.

Assessing risk and uncertainties: The variable with low sensitivity are more risky so need to be assessed and considered thoroughly. Also, if there are uncertainties that certain variable changes beyond tolerable limit, it is worth not undertaking such project.

Optimizing revenues or cost control: If revenue variables like selling price or volumes are sensitive, they should be further optimized. For example, conduct value engineering to assess non-value added features from the product so that its cost can be reduced and, ultimately its selling price.

Optimum allocation of resources: The cost of sensitive variables can also be reduced by allocating necessary resources that drive costs optimally. For example improve quality of production so that waste is reduced and number of inspections can be reduced which will reduce allocation of inspection costs of the product.

Scenario planning: Sensitivity analysis in itself is based on what-if-analysis. We can forecast different scenarios for each variable to change and see whether such change will exceed the tolerable limit of such variable.

Hey there, I appreciate you posting great content covering that topic with full attention to details and providing updated data.

I enjoy looking through a post that can make men and women think. Also, thanks for permitting me to comment!

I have read so many articles or reviews regarding the blogger lovers except this paragraph is in fact

a pleasant post, keep it up.

It’s nearly impossible to find experienced people on this subject, however, you sound like

you know what you’re talking about! Thanks

Wonderful goods from you, man. I’ve take into account your stuff prior to and you’re

just too fantastic. I really like what you’ve acquired right here, certainly like what you are stating and the way through which you

are saying it. You’re making it enjoyable and you still care for to

keep it wise. I can not wait to read far more from you. This is really a great web site.

Your style is so unique in comparison to other folks I have read stuff from.

I appreciate you for posting when you’ve got the opportunity, Guess I’ll just bookmark this site.

It’s going to be finish of mine day, but before end I am

reading this fantastic article to improve my

knowledge.

It’s an awesome paragraph designed for all the online viewers;

they will obtain advantage from it I am sure.

I was recommended this blog via my cousin. I’m not certain whether or not this submit is written by

way of him as no one else understand such precise about

my difficulty. You’re wonderful! Thanks!

I’m really inspired along with your writing skills and also with the structure on your blog.

Is that this a paid subject matter or did you modify it yourself?

Either way keep up the excellent high quality writing, it is uncommon to look a

nice weblog like this one today..

I really like your blog.. very nice colors & theme.

Did you design this website yourself or did

you hire someone to do it for you? Plz answer back as I’m looking to construct my own blog and would like to find out where u got

this from. thanks

Spot on with this write-up, I really believe this amazing site

needs far more attention. I’ll probably be returning to read more, thanks

for the info!

My brother recommended I might like this web site.

He was totally right. This post truly made my day.

You cann’t imagine just how much time I had spent for this information! Thanks!

I do not even know how I ended up here, but

I thought this post was good. I don’t know who you are but definitely you are going to a famous blogger if you aren’t already 😉 Cheers!

I really appreciate this post. I’ve been looking all over for this! Thank goodness I found it on Bing. You’ve made my day! Thx again